Following Vikram Solar’s recent public listing, the renewable energy industry in India is exploding. The company, which is among the biggest producers of solar PV modules in India, is making headlines for its eagerly awaited initial public offering and subsequent market performance. We’ll analyze the IPO listing, share price movement, company history, valuation insights, outlook for the future,

and things investors should watch in this blog.

Table of Contents

- Vikram Solar at a Glance

- IPO Details & Market Debut

- Share Price Movement & Valuation

- Growth Highlights & Strategic Moves

- Risks & Analyst Views

- Tags, Internal Links, and Embed Resources

- Frequently Asked Questions (FAQs)

Vikram Solar at a Glance

Vikram Solar Limited was founded in 2005 by Gyanesh Chaudhary and has its main office in Kolkata. With a focus on PV module manufacturing, EPC (engineering, procurement, construction) services, and solar infrastructure operation and maintenance, the company is a major player in the Indian solar energy market.

Its production capacity has increased to roughly 4.5 GW over time. West Bengal and Tamil Nadu are home to manufacturing facilities. Among its noteworthy achievements are the commissioning of India’s first floating solar plant in Kolkata and the world’s first fully solarized airport in Kochi.

IPO Details & Market Debut

- On August 26, 2025, Vikram Solar debuted on the stock market. The following are the main IPO highlights:

- Total IPO size: ₹2,079.37 crore, comprising ₹579.37 crore through offer-for-sale mintUnivest and ₹1,500 crore through fresh issuance.

- Price range: mint shares range from ₹315 to ₹332.

- Overall, the subscription was oversubscribed by about 54.6 times; QIBs were 142×, NIIs were 51×, and retail was 7.6× .

- According to The Economic Times, the Grey Market Premium (GMP) is estimated to be around ₹41, indicating a listing price of about ₹373 (approximately 12.4% above the upper band).

- Price at listing:

- 2.4% over ₹332 (BSE: ₹340) Moneycontrol mint, The Economic Times.

- NSE: ₹338 (1.8% premium) Moneycontrol mint, The Economic Times.

Share Price Movement & Valuation

Post-listing performance:

- The share price experienced a robust surge, rising approximately 9.2% and trading close to 12% above the initial public offering price. On the BSE, it peaked at about ₹371.25. The Economic Times The Economic Times.

- NSE: ₹357.50 (+7.68% over IPO) and BSE: ₹356.45 (+7.36%) mint at the end of the day.

Real-time insights:

- Screener: ~₹356, down ~6% on the day of listing.

- Finology: Finology Ticker: Intraday range: Low ₹333.65; High ₹381.65; close ₹363.70.

- Trendlyne: By mid-afternoon, the share was trading at ₹364.40 with a high volume of about 76.7 million shares on Trendlyne.com.

- Metrics for Moneycontrol: VWAP ₹362.28; daily volume high; market capitalization ~₹12,892 crore.

Analyst commentary:

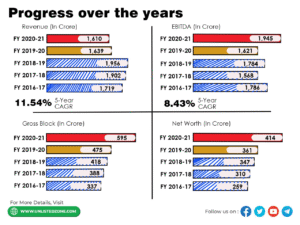

- Good financials: EBI TDA increased at a 62.6% CAGR, revenue increased at a ~28.5% CAGR (FY23–25), and margins increased from 9% to 14.4% mint.

- Valuation: Post-issue market capitalization was approximately ₹12,009 crore mint, and full-year FY25 earnings were valued at ~85.8× P/E.

- Market positioning: Mentions Atmanirbhar’s advantages, robust order book, and focus on renewable energy, which are seen as long-term investments in clean energy, according to mintEnergyworld.com.

- Caution: Analysts advise a stop-loss of between ₹320 and ₹325 mint because the high valuation calls for patience.

Growth Highlights & Strategic Moves

Manufacturing: With additional plans, the capacity will be increased to 3.5 GW (e.g., 3 GW cell manufacturing in Tamil Nadu; U.S. facility).

Exports & Projects: Providing flagship projects such as the 397.7 MW NTPC Gujarat, the 393.9 MW NLC Gujarat, the 251.25 MW GIPCL Kutch Hybrid Park, and the 1 GW JSW subsidiary order, according to Wikipedia.

Global reach: BNEF-ranked Tier-1 manufacturer with solid R&D credentials (Wikipedia).

Risks & Analyst Views

Principal hazards:

- High valuation: P/E close to 80–90× indicates high expectations for mint.

- Client concentration: It lacks a variety of revenue sources, with over 77% of revenue coming from the top 5 clients and over 98% from PV modules.

- Execution risk: Plans for significant capital expenditures and expansion call for careful execution.

- Policy dependency: The expansion of domestic solar is largely dependent on advantageous government incentives, such as PLI programs.

Analyst’s opinion:

- It is advised to hold with a cautious stop-loss close to ₹320–₹325 mint.

- Long-term potential: Considered a structural factor in India’s trajectory of solar growth.

- Investor sentiment: A robust rally on the first day of trading suggests optimism about future prospects, which is restrained by high prices.

Links & Include recommendations:

Internal links:

- About Vikram Solar

- IPO & Listing

- Performance & Valuation

- Growth Strategy

- Risks & Analyst Perspective

Include recommendations:

To visually represent capacity, IPO hype, and company milestones, use the image carousel at the top.